(I forgot to hit send on this post, so it’s coming out late. Oops)

This last week wasn’t a great one for my portfolio. I remain positioned very short and in this short week as the market’s had what I believe to be a very short lived rally, I took a bunch of paper losses.

No changes to the portfolio this week. I’ll hold into next week as I expect the market to begin to soften. The good news is with the VIX coming down, I may be able to at least get out of my April VXX credit spread for a scratch, or maybe a few bucks. We will see 🙂

As expected, volatility is starting to come in a bit and the markets are acting a bit more “normal” during this time of economic and societal uncertainty. This week we had some actual 2 sided action… markets that for all intents and purposes are looking like one would expect! Check out the chart of the /ES – it’s starting to look normal trade (just larger ranges).

You can see the IV come back in over the past few days as well as all of the momentum indicators.

This week I started to dramatically pivot my trading posture back to “normal” and have moved away from being a net purchaser of options to a net seller of them again. I still have a few debit spreads or outright buys that I will do for appropriate catalyst events – otherwise it’s back to selling premium as the market likely grinds lower for some time.

All of my portfolios are bearish in their stance with my long term accounts in almost all cash or cash equivalent investments.

I have positioned my retirement accounts; 401(k), IRA etc… into highly defensive postures. Most of this occurred before the drop began in late Feb and I adjusted a bit more aggressively during the first 2 weeks of the market declines.

As a total side note… I really dislike limited investing vehicles – especially in times of crisis… 2008-2009 was very frustrating to me as well, so much lost opportunity for profiting on both sides of the trade. My 401(k) has some really great options for bull markets, but in bear markets it’s meh.

For the speculative accounts, I am short delta and getting back to long theta positions. I do have a host of hold over “debit spreads” mainly in the SPY’s that expire in the April cycle – depending on the market movement over the next week I may sell these off for some realized losses.

I captured about 4% in realized profits for the total portfolio and remain about 25% allocated. I’ll be moving that up in a measured pace over the next couple of weeks.

Current positions:

EFA – Debit Call Spread, likely to expire worthless

OIH – Credit Put Spread 5/4 in April, this position will likely get rolled out over the next week or so. I don’t really want to get assigned OIH and would prefer to simply carry the spread forward for a small debit.

OPK – Long stock, this one is meh and I’m only holding it as I expect it’ll come back close to my purchase price at some point during this Coronavirus time. OPK is a testing firm and some news shortly should again cause them to pop. I’m in at $1.90 and it’s trading at $1.17. Normally I don’t do tiny stocks like this, but with the virus the opportunities where really good.

SPY – Lots of positions, net short. The vast majority of my positions here are for the April cycle. I have put spreads as low at 175/170 (unlikely to be profitable) and some as close as our current 245 or so. I also have a bunch of credit call spreads with the low strikes being around 263 and up.

For SPY I’ve been opening credit spreads, and then tossing a GTC buy back order at 50% profit. They are hitting in a matter of days given the amount of movement we are seeing which is pretty nice.

VXX – I’m still short vol with VXX and I’m not sure the April position is going to come in for me. I may need to roll it out if I can do so for a reasonable price. April is 37/40 on the calls and May is 40/45. We’ll need a pretty big vol crush for the April positions to pan out.

XLP – Credit Call Spread at 57/62, just a bearish spread.

XLU – Credit Call Spread at 56/61, same as above.

I got in and out of a few positions this week in /ES, GILD CCL, HTZ, WTRH, TSN and T – a mixed bag but overall profitable.

I was able to get my SPX selling going again as well, and they had a perfect week. I’m glad to get those started up. Scaling is not on contract size, but on spread width for now. I am seeing slightly better fills and less slippage using that method.

Here it comes! Unlimited QE and trillions of economic stimulus was unleashed this week.

Unsurprisingly, the markets responded in kind and rallied hard. I don’t expect this rally to hold, and am positioned to the short side.

I really didn’t do a lot of trading this week outside of some futures positions to profit from the expected stimulus package passing and some debit call spreads on the SPY/QQQ as I expected the market to boost higher.

These were all exited for some decent profits which have offset the marked losses I have on all of my long put spreads.

I did get burned a bit on some poor timing on /ES and /NQ trades in the middle of the week but that’s the nature of trading futures 🙂

Coming into the end of the quarter I expect the markets to be generally softer, but the extreme movements we’ve seen should start to diminish. The VIX is starting to come in a touch, although there is still a lot of volatility priced in.

My portfolio is as follows:

SPY – short, very short.

EEM – breached put spreads that will likely need to be rolled or otherwise managed.

EFA – long credit spread – it’ll be a max loser

OIH – short put spread, breached and will need to be managed

QQQ – short call spreads

VXX – short call spreads, all breached but likely going to be coming in over the next couple of weeks

Stay safe and trade with appropriate risk. I’m about 25% allocated currently and expect to start to increase that over the next month or so.

With all of the human tragedy happening around the world right now, these posts seem somewhat trivial. Before getting into the details of trading and my weekly rhythm; I’d like to start with a quick prayer

Heavenly Father, in these turbulent times we turn to you as our source of hope and strength. God we are thankful for your provision and your love. For your unending mercy and grace. We thank you for the gift of salvation that you have provided to us, and for accepting us in our brokenness every day. You’ve asked us to bring our burdens to you, and Father we do that today. Lord help us to turn our focus to you, and Father we ask to that settle our hearts and minds brining peace. Thank you Father for your love and provision. Amen

While I don’t talk about it much on this little blog, I’m a follower of Jesus and he is my hope and strength in these difficult times. The world is a crazy place and will likely continue to be that way until He returns. I’m super thankful that the God of the Universe has decided to offer us a hope for eternity.

This week was yet another hard down week in the markets. The fed acted multiple times and it’s just been crazy! This week I also spent the entire week working from home using video conferences as my primary method of working. It was exhausting given the amount of change that is to my normal rhythm.

For the week, I didn’t trade a ton, but I did do a few things. I had a bunch of March expiration positions that closed out across most of the equity names I have in. Some I simply let expire, and a few I closed to limit risk in the unlikely event of an upturn.

My positioning is still firmly bearish, and I’m short /ES over this weekend.

Having close access to my trading platform during the week was weird for me. I opened a bunch of short /ES positions in the overnight or early am sessions that I closed early for losses this week. It was good to have quick access to glance at market activity. It seems my loss aversion, given all the uncertainties around us, has gone up a lot. That’s a shame, because the initial decision to get short was right each time. I exited early for losses that didn’t need to be realized. This was a good (although expensive session) this week and I will have to adjust accordingly as the weeks go on. I expect to be working from home for the foreseeable future and there will be ample opportunities in the coming weeks that require patience to let them play out in these exceedingly high volatility markets.

With the March cycle closing on Friday my portfolio is down to only a few symbols:

/ES – Short

EEM – Iron Condors, all breached in the April Cycle. These will likely need to be closed in the next few weeks.

FXI – Very wide Iron Condor, March 27 Expiration – currently near the put strikes. China appears to be recovering from the initial impacts of Coronavirus. If they can hold that for the next week I should be able to close this for a small profit.

IWM – Short Call Spread March 27; this should be a max winner. I’ve got a GTC in to close it for $0.02.

MNK – Long stock. It’s a small position, hopefully it plays out nicely this week otherwise I’ll cut it. I’ve got GTC’s in for my targets if it happens to bounce.

OIH – Short Put Spread 5/4, April Expiry. This one is going to be a lotto ticket. If I end up long OIH at 5, I’ll likely take the shares. Over the longer term, OIH should come back up above 5 and I’ll sell covered calls over this if needed.

OPK – Long stock. Again, a small position and I’m holding it for Coronavirus news. I’ve got GTC’s in for my targets if it happens to bounce.

SPY – I’m all wrapped around SPY, net VERY short. This is driving almost all of my portfolio delta right now. I’ve got a lot of put debit spreads, some for next week and some for April. If we get a strong bounce on fiscal stimulus news, I’ll send a bunch of call spreads as well.

VXX – I’m still short vol on VXX. This credit spread is a 37/40 so it’s way in the money. This isn’t a max loser yet, and I’ll plan to hold onto it on the chance that vol settles over the next 4 weeks or so. I will consider get into more VXX short positions this coming week.

Anyhow. I’m burned out from the week, so that’s all I’ve got for now. Stay safe, physically and financially!

The market’s moved to limit down late last night, this morning when they opened up we immediately hit the circuit breakers for the 15 minute trading halt.

I believe we have a reasonable chance to end up with a trading halt today given the degree of uncertainly in the market place. That would be a 20% drop in the overall markets. Given the massive ramp up Friday, that would simply require the markets to give back Friday, and have another Wednesday or Thursday from last week.

I am certainly not hoping for such a drop; however uncertainty has hit a peak and with that markets will respond with flight and fear.

At a minimum, I expect markets to close >10% down today (absent a fiscal package) from the Friday highs.

The organizations that I am engaged with in a leadership capacity are all shuttering non-essential services and finding alternative ways of working. We see similar things happening across the world; and until that all shakes out and we understand what the future may look like, I expect markets will simply continue to drop lower.

My current expectation is that we will see 1800/1750 on the SPX sooner rather than later.

This evening, the Federal Reserve dropped the discount rate to 0%-.25%. The FOMC met this weekend and have cancelled the planned meeting later this week.

I’m not extremely surprised; however it’s not going to fix the underlying problem.

As I type this, the futures markets are limit down effectively across the board. With an almost 10% up day on Friday, I expect we will see the next leg down starting tomorrow.

Fiscal stimulus is certainly on deck soon, however I’m not sure it will do much to mitigate the downward pressures that we are experiencing due to the Coronavirus. Once a fiscal package is passed, I expect it will provide a near term rip higher, but that’ll be short lived.

As of right now, the FOMC is holding pat on not going to negative rates. The Fed is very likely going to expand QE is a material way, this is just the first step.

Fox Business asked a great question that the Fed chair dodged expertly on the call regarding buying “other assets” simply stating that they do not yet have the legal authority, and are not asking for it yet.

First off, my heart goes out to the millions of people around the world who are impacted by COVID-19 and the health, social and economic impacts it has created. My family is impacted, however not anywhere near as much as those in China, Europe and other parts of the world. We will continue to pray for all impacted as we collectively work through this challenging time.

On March 1st I wrote:

Last week marked one of the most aggressive, and orderly sell off’s that we have ever seen in the markets. It was however not a crash.

What you just witnessed on during the week of March 8-14 2020 was indeed a crash. The global markets are panicking and have no idea what the future brings. I’m not sure this is the only one we are going to see in this cycle – so keep alert!

Treasury marketings are starting to show extreme signs of stress leading the Federal Reserve to unleash 1.5 trillion in capital to aid the smooth flow of bond markets. (wsj: Fed to Inject $1.5 Trillion in Bid to Prevent ‘Unusual Disruptions’ in Markets) Fiscal stimulus is on the way (almost certainly) over the next week and the fed will very likely cut the benchmark overnight rate by another 50 bps during its upcoming meeting.

As for my trading, this week wasn’t extremely active however I did make some adjustments and moves. The SPY puts I bought last week played out very nicely and 1/2 were sold for a about 115% on Monday while the remaining 1/2 was sold on Thursday for 700% via GTC orders – that was shocking too me. Those puts have broadly offset the losses that I experienced at the beginning of this down move by expecting chop way too early.

On Wednesday night, when the NBA cancelled the season I also jumped into a bunch of /ES shorts that played out very nicely. Unfortunately, I bought those back a little early and then decided to continue to play downward momentum over Thursday night. The gains from Wednesday were wiped out during the limit up move.

As of this moment, by speculative portfolio is basically neutral. I have two long stock positions is OPK and AGRX that I am looking for upward momentum in; I will likely cut those loose this week if they don’t start to move in my favor.

On Friday I sold a host of bear call spreads on DIS, IWM, AAPL, DIA, CCL and a few others.

My only short vol position (which is getting creamed) is VXX April 37/40 Calls, with the VXX at 43 this one is looking pretty nasty right now. With what we are learning about the virus and the impact is it having in other nations, I’m not confident this VXX position is going to turn around.

I’m also in a TLT position that has gotten a little better after TLT came in hard last week. It’s still completely breached and if an opportunity presents itself on Monday to get out – I’ll be doing that. I expect bonds to continue to rally over the next couple of months as our economy is continued to be stressed.

SPX selling was solid this week; although I didn’t do it every day. Given some obligations both personally and professionally I was not comfortable with entering positions on Monday or Friday. I did enter on Wednesday and it was 100% profitable. Backtesting shows that I would have had profitable trades on Monday and Friday as well. I’ve adjusted my risk management strategies for this market which include being very careful on the call side of the short dated options. Pullbacks are much more vicious than selloffs in this type of an environment – they also happen at a time that my strategy is very vulnerable too.

This weekend I’ll be putting together my game plan for the next few weeks. My belief is that things are going to get a lot more challenging before they turn around. There will be some particular names that should do very well in this challenged environment, however there will unfortunately be many that will be very very impacted.

Rally’s will continue to be strong – however I believe they will be short lived.

I sold most of my “doomsday” hedges too early into this cycle, so I plan to assess other ways to adjust for severe economic contraction.

At some point, hopefully much sooner rather than later, there will be a tremendous opportunity to invest into strong companies and growing economies as our world recovers from the impact of this current time.

Monday looks like it’s going to be quite the ride. As I type this late Sunday evening, the /ES dropped like a rock and is basically pinned to limit down; treasuries have fallen to sub .5% on the 10 year, the 30 year is below 1% and oil has cracked $30…

Absent some sort of intervention, we are experiencing a real crisis and may see a true crash tomorrow and into this week.

Circuit breakers:

Assuming the Fed doesn’t jump in tonight, I wouldn’t be shocked to see a Level 1 halt, possibly even a level 2 halt tomorrow. For those of you that aren’t aware of these basically they work as follows:

Level 1 – At a 7% down move, trading stops for 15 minutes (if it happens before 3:25 PM EST)

Level 2 – At a 13% down move, trading stops for another 15 minutes (if it happens before 3:25)

Level 3 – At a 20% down move, trading is halted for the rest of the day.

If you want more info: CME Group has futures info here, CNBC did a piece a few years back here and of course the SEC has the final word here.

Given the recent intraday price movements we’ve seen, and that /ES futures are locked limit down at 5% on the Globex session, another 2% at the open seems very possible.

The speed and size of these moves over the past week have likely resulted in liquidations and a few firms “blowing up” as they cannot cover margin requirements due to vol expansion, gamma risk and all of the related problems that come with these massive moves. With /CL, /ZN, /VX and /ES doing what they are doing tonight – more liquidations tomorrow seems very possible – and that means more downside pressure.

Be safe and manage your risk sizing!!! As I write this:

It’s not looking good for tomorrow’s opening, or likely the next couple of weeks…

This post is a little late – it’s been a busy week and weekend!

Last week was just downright crazy in the markets. It seems like the week took a month or two to finish given how big the moves are and how crazy the trading has been.

On Tuesday the Fed cut rates by 50 bps; which was either a brilliant move or, more likely, a massive warning sign that things are going to get much worse before they get better. My guess is they do another 50 bps this month; I’m not sure they will wait until the meeting on the 18th, but that is where I would be placing odds.

Over the past 7 days, I’ve done a tremendous amount of position adjustment and changes to my risk profile again. The travel industry is continuing to get hammered (it doesn’t look like it’ll stop anytime soon) as major corporations start to cancel conferences and implement restrictions. The put spreads I had against these names were all too close to handle that kind of demand destruction, so I’ve mostly closed them down. Those companies are typically highly leveraged and operate on relatively thin margins when things are going well, so there will likely be continued selling pressure across those names. I will consider opening calls spreads with a shorter term bias on those names as time goes on.

This week, my focus was on a lot of COVID-19 short term plays; typically in the medical sector for those that are working on treatments, testing or the like. These names are showing tremendous volatility and opportunity for short term speculation.

I remain short vol via VXX and UVXY however those positions are starting to look less favorable as the weeks grind on. My UVXY positions are out in April so they have a decent chance of coming back in, however the VXX expire March 20th and are well under the current VIX readings. Given the likely timing of the spread of this virus (weeks and months vs. days), my expectation is that the VXX positions are going to be just too early for vol to come back in. Time will tell.

To manage against the tremendous amount of movement in SPY and the continued expansion of volatility, I’ve flipped to be more of a purchaser of SPY vs. a seller of it for now. I’ll evaluate this stance weekly for the next few weeks and eventually swing back the other way to sell premium. For right now, the moves are simply too large and vol expansion is simply too big to see these positions make money in the short term.

Typically I have longer term spreads on that are simply playing for theta decay and moves insight implied vol. I still have a bunch of April call spreads on across DIA, XRT, XHB etc… however, I haven’t done the put side of these and don’t plan on it to keep a bearish tilt in the portfolio from a selling perspective. I did round off my IWM and EEM positions to be neutral.

Quick portfolio review:

Long: AGRX, BCRX, NAK, VSTM, OPK

Neutral: EEM, IWM, CMG, WYNN, CCL, FDX

Short: DIS, DIA, XHB, UVXY, VXX, MGM, XRT

I’ve been using SPY as a scalping vehicle and currently have a slightly long delta position due to the current market movement – dynamic delta has been very dynamic recently. I’m long both puts and calls to scalp volatility spikes as well as have a normal neutral VERY WIDE iron condor for April that I’ve legged into.

Next week – I really have no idea where the market goes. Given the recent events in Italy and across the US; I expect that we’ll open the weekend with futures down and have more selling pressure. The market’s don’t look healthy with liquidity all but gone and I expect to continue to see massive moves in the major indexes for the next week(s).

My personal opinion here is once we get some degree of understanding of the true risk of COVID-19; the markets will adjust accordingly. For right now, it’s a massive cone of uncertainty with more downside risk than upside in my view.

My SPX selling strategy had its first full loss this week. On Wednesday, my short call spreads where at 3125/3130. These where sold when the market was already up 40 or so points, and had about 90 points of head space above them.

As you can see from the charts below – SPX ramped just over my top strike into the close running about 20 points higher in 10 minutes or so.

Then immediately after the close, simply dropped back down 20 points so so.

There isn’t much one can do with a situation like that. However, it is interesting to see how the backtesting played out perfectly on this one. My testing had shown that the biggest risk to these positions is on massive up moves.

The good news is that even with the loser on this trade, I’m still up on a unit basis for the year. Overall down due to scaling, but that’s okay. I’ll keep testing and if this strategy can survive a market like this – well good grief it should be able to survive anything!

Last week marked one of the most aggressive, and orderly sell off’s that we have ever seen in the markets. It was however not a crash.

Market’s do crash, and when they do it is disorderly and pricing moves are vicious. Friday was the closest thing we saw to a crash, however the buyers stepped in (my guess is to cover their short positions) over and over throughout the day. If we drop more than 5% in a day we are in a real true crash type of situation – we have seen an orderly repricing of risk.

However, liquidity appears to be drying up, and the market for all intents and purposes appears to be ready to simply puke on itself sometime in the next few weeks. Futures this weekend opened with the /ES down another 30ish points; I wouldn’t be surprised to see that continue to have downside pressure unless something changes overnight – possibly bringing another 100 point down day in the SPX.

News of the COVID-19 spread is all negative. The United States experienced the first death directly related to COVID-19 and there appears to be a cluster of new cases forming on the east coast. Given that information, along with the news that the Washington cases could have been spreading for weeks it is a virtual certainty that we will have a massive spread of COVID-19 across the US at this point.

If the future response to the spread in the US looks anything like it has in other countries, we are in for severe demand shocks and quarterly earnings are going to tank for many, many firms. The market understands this, and appears to be absorbing this possibility; if it begins to materialize… look out below.

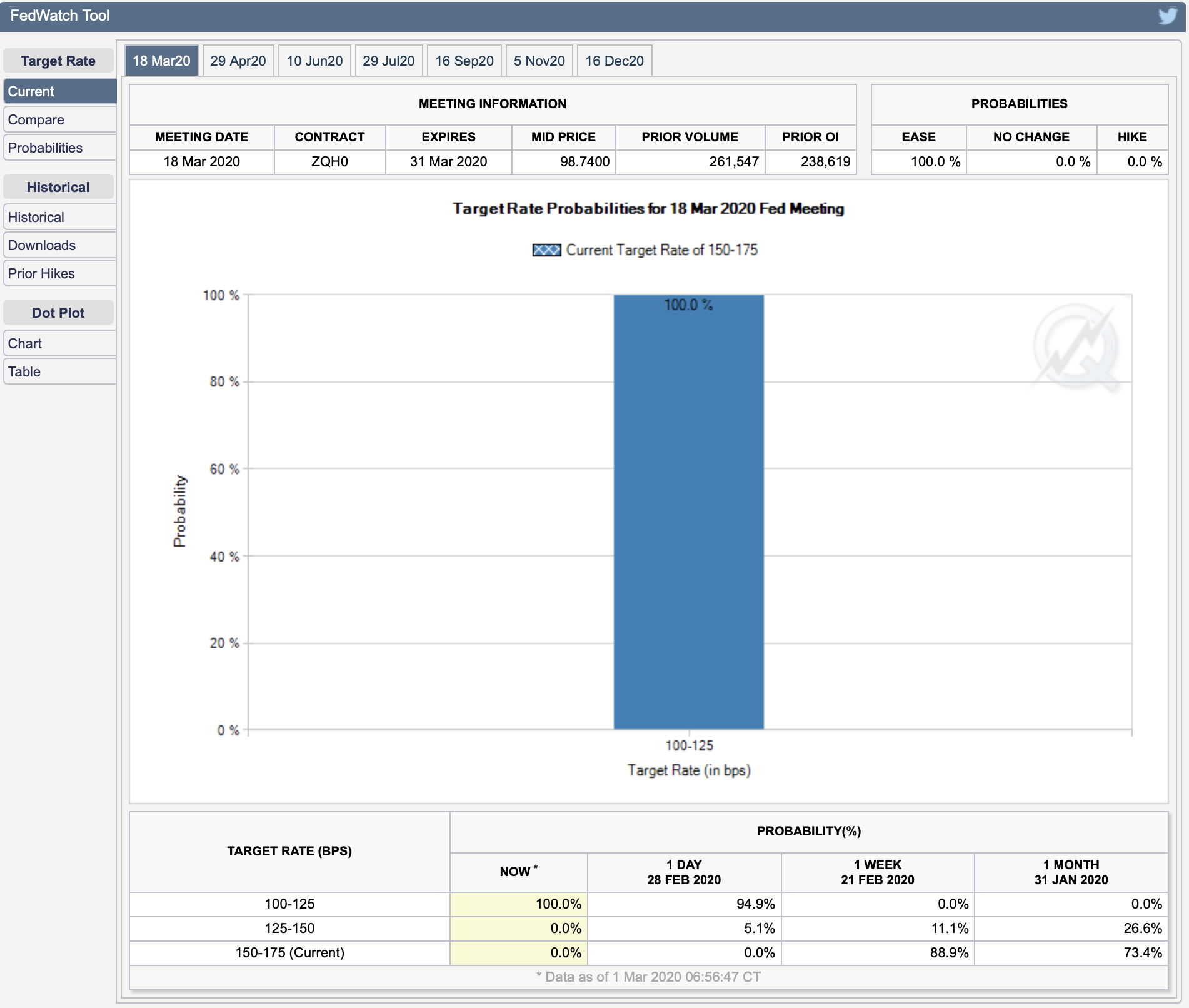

Markets are pricing almost 4 rates cuts in at this point – and honestly, I was a bit surprised that the Fed didn’t step in before the futures opened this weekend. While central banks can’t cure a virus, they can inject liquidity, lower rates and show accommodative policy to ease financial frictions.

The CME has a nice little tool called FedWatch – it’s pricing a 100% change of a cut at the next meeting…

My guess, in the next seven days – central banks across the global begin a coordinated effort to “ease” financial conditions. That leads to a wicked near term jump in the markets and a tremendous selling opportunity.

I’m planning to continue to remain nimble and trade the tape as it develops.